Benjamin Beck, CFP®

Benjamin Beck, CFP®Have you ever been in a conversation with someone, and they say something that strikes you as totally wrong, or even bordering on ridiculous? Something that isn’t even factually correct, but it’s said with such conviction that it sounds like it may be? I experienced a scenario like this not too long ago.

I was attending a conference with another member of our team, along with folks from businesses around the country. One night, at a dinner during the event, I was sitting next to this man who was a financial advisor. He was probably in his mid-forties, and by his description, he had a very successful financial practice with six or seven people in his business.

The conversation turned to the current economy, rising inflation, and the general feeling of uncertainty. As he shook his head, he said something like (I’m paraphrasing), “You know the gist of it is that inflation doesn’t really matter for me or most of my clients … when you break it down, our best clients have plenty of money, and they don’t really need to take any risks in retirement.” He then concluded by saying, “Inflation only affects folks who are living paycheck to paycheck.” I couldn’t believe he was saying this so matter-of-factly like this was the truth and that’s all there was to say about it.

Now, let’s say it’s me who’s sitting across from a couple who has done well financially, maybe they have a pension and/or a few million dollars in their retirement accounts. I may ask them how confident they are about their retirement income, and they may even say, “Well, we’re not spending enough money to the point that we’re concerned about running out.” As I continue to ask them questions, if they say that losing their independence and dignity in retirement is not a threat to them, or is of no concern to them, I will tell you that I think they’re either lying to themselves or lying to me.

Preparing For Retirement Requires Financial Honesty From Both Sides

As I sat next to this advisor at dinner during this conference, I thought, my goodness, outliving one’s income is not just a possibility today for many people. I believe it’s almost an inevitability! Many people — if they do not plan correctly — face the high likelihood of outliving their income. I can't think of anything more misleading than saying that “inflation doesn’t really matter” when you base a potentially 30-year-plus retirement on the adequacy of a client’s retirement income today to satisfy their spending needs in the future.

At Beck Bode, we test the thesis by asking our clients, “How much income do you think you'll need in the first year of retirement to satisfy your lifestyle?” In our experience, most clients will respond with a number that is below their current income. That’s because most people assume that when they retire, they will end up spending less money because they’re not doing this, that, or the other. OK, fine. Whatever income it is that they think they will spend, we then compound that at 3% for the next 30 years (assuming that this hypothetical client is around 60 years old, and assuming they live for another 30 years).

Once we do this math, for the most part we see the lines cross: we see their income need (meaning their expected spending) rise above the flattening income that they’re receiving.

We see this happening for most of the people we meet. And I'm not talking about people who live paycheck to paycheck, these are people who have resources. Somewhere between the 10th and the 20th year of their retirement, we see a huge shift in their financial picture based on the compounding effect of inflation on their expenses. And once that shift happens, when their expenses exceed their retirement income, what alternatives you think they have but to dip into their original investment? When you start dipping into your original capital, you hope to die before it's gone. Well, that's not much of an alternative!

Poor Financial Planning Can Lead to a Retirement Crisis

Let me tell you what we believe.

We believe you have an alternative and that is to own equities from the get-go. Over long periods the consumer price index has historically compounded at a growth rate of about 3% annually on average. Now the S&P index — the dividends alone, over long periods, have compounded at an average annual growth rate somewhere between 5% and 6%. The only way I know for a client to not lose their dignity and financial independence in retirement is to be invested in equities.

But I believe this financial advisor sitting next to me is missing this entire piece of the retirement picture. He is missing the staggering effect that the erosion of purchasing power over a three-decade period can have on a retirement! Just because his clients have a couple million in their account today and they’re telling him they’re not spending more than a certain amount, he’s willing to take a pass on telling them the truth of the situation.

Now, I can't say that the downturn that we started to experience in 2022 is over, or in what direction oil prices will continue to move, or when things will turn around. But there's no shame in that, right? Because nobody else can, either. There's no set of commentators on CNBC or Fox Business or any other channel that can tell us that with any kind of accuracy. What I can say with certainty, though, is that for every person or couple going into retirement, one of two things is going to turn out to be true. They're either going to outlive their money, or their money is going to outlive them.

Everyone Feels the Effects of Inflation

Will you outlive your money? Or will your money outlive you? This is a matter of your independence and dignity that needs to be considered seriously. You will need to support your lifestyle every single day with your retirement income. The fact of the matter is that the cost of everything will likely rise throughout your 30-year retirement every year. When your living costs rise, your retirement income must also rise at the same rate or higher, or else you will end up needing to consume your initial investment. That’s when people run into trouble.

So, we know the consumer price index has averaged about 3% compounding over long periods of time. Of course, more recently, we know that living expenses for many have gone up significantly. According to this guy who was sitting next to me, inflation shouldn’t matter to you or me if our income is above a certain level, or if we have a healthy cushion of assets to rely on. But I submit that $6 for a dozen eggs affects me when I am providing for four kids. A team member of ours who has six kids has done a fantastic job showing the effects of inflation on his grocery bill by posting them on Instagram.

It doesn’t matter how much money you have; I believe that inflation affects everybody and even more so someone who will be retiring soon or has already retired and is staring at 30-plus years of having to fund their retirement with a pool of money they created in the past.

As we just mentioned, the dividends of the S&P 500 have chugged along, compounding at about 5.5% over time, on average. We know that past performance is no guarantee of future results. We know that dividends don't rise every single year like that, but on average that's what they've done.

In our view, the rising income that dividends have historically produced are much better at preserving real purchasing power for investors than fixed income vehicles. But that’s not what I believe this advisor was telling his clients. He is telling them that they can buy dignity and independence with the fixed rates of interest that bonds and CDs can provide.

Where is his attention when he says things like this? I believe his attention is on the short-term gyrations on the market. Why else would he tell his clients that they don’t need to invest predominantly in equities? Why else would he tell them, “You don’t need to take a risk.” I believe he’s telling his clients, “Inflation won’t affect you because you don’t live paycheck to paycheck.”

The Existence of Inflation Emphasizes the Importance of Retirement Income Planning

History has shown us that the more one can rely on the dividends of great companies in the United States and around the world, the better chance one has to fight and prevail against the inevitable erosion of purchasing power over time. And the more one relies on fixed rates of interest paid by bonds and CDs, the less able one may be able to keep up with rising living costs, and the more one may need to dig into one’s capital to fund a retirement. Within a properly structured financial plan, and with the right investment portfolio to fuel that plan, it is our belief that growing dividends play an important role in creating funding for the future: helping retirees live on for upwards of three decades, without losing their dignity and financial independence.

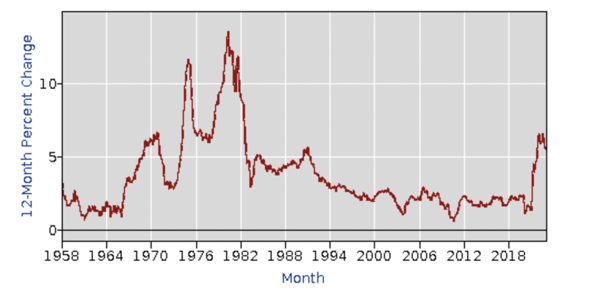

It's my obligation as a financial advisor to ask you, the investor, to consider … what will your income be in retirement? How much income will you need in your first year of retirement? Will it be enough to cover your expenses? And if you’re already retired, I ask you, how much income do you think you'll need 10 years from now, or 15 years from now? To ignore the erosive impact of inflation is to look away from reality. I don’t need to convince you of this, all you have to do is look at a chart from the U.S. Bureau of Labor Statistics showing historical inflation trends.

CPI for All Urban Consumers in the United States (1957-2023)

Source: U.S. Bureau of Labor Statistics

Because we are not in the convincing game, we are not here to look away from what is real and happening all around us. We're in the common sense game. Common sense tells us that for most Americans, outliving their income in retirement is a distinct risk, and it will take proper financial planning to make sure that that doesn’t happen. Don’t be fooled by anyone who tells you differently.

Learn more about Beck Bode’s investment management services.

Ben Beck is Managing Partner & Chief Investment Officer at Beck Bode, a deliberately different wealth management firm with a unique view on investing, business, and life.